The early bird catches the worm

In an investment context, gold, silver, platinum and palladium are the most commonly used precious metals. Platinum and palladium are almost exclusively dependent on industrial demand and are subject to enormous price fluctuations. They are therefore more suitable for speculative investors and less suitable as portfolio stabilisers. Gold and silver fulfil this function better. Compared to gold, silver is more volatile and more dependent on industrial demand. In a portfolio context, silver has less good diversification properties than gold. While gold has a negative correlation with equities, silver has a slightly positive correlation. Gold thus stabilises a portfolio and can be seen as a kind of portfolio insurance. The fact that the silver price has lagged far behind the gold price speaks in favour of silver in the current environment. Silver investors are betting that this gap will close again. It is difficult to say whether this will be the case. Some "laws" relating to gold and silver appear to be suspended at the moment. One example of this is the breaking of the negative correlation between real interest rates and the gold price. This has a lot to do with the current geopolitical and economic situation and presumably also with the fact that gold can build on its historically outstanding significance in uncertain times. Gold is deeply rooted in society. It has a religious character, guarantees monetary stability and can be found in a rich vocabulary of proverbs: "Home and hearth are worth their weight in gold" or, more critically, in Goethe's Faust: "After gold urges, On gold depends, But all we poor" or the praise of the early riser: "The early bird catches the worm". The following comments focus on gold and the question of how it should ideally be used in a portfolio context.

Gold has had the risk profile of equities since 1971

The real (inflation-adjusted) return on gold in USD was 0.76% per year for the period from 1900 to 2022. Compared to US Treasury Bills, gold outperformed by 0.31% per annum for the same period. However, gold was a key component of monetary policy until Bretton Woods was cancelled in 1971. As long as the gold standard was in force, the purchase of gold was partially restricted and the price was fixed. With the abolition of the gold standard, the price of gold became a market price. This is one of the reasons why the fluctuation range (volatility) of gold has skyrocketed since 1971 and is now on a par with equity investments. The same applies to the price development of gold, which has been around 8% per year since 1971 compared with 10.7% per year for US equities. However, it should be noted that the data series for precious metals do not reflect the storage costs of physical storage. The actual returns on precious metals are therefore lower than these long-term figures. Gold therefore has a lower return than equities with a similar level of risk. If only these parameters were considered, gold would not necessarily be included in a portfolio. However, gold also has other characteristics that make it interesting. Gold is crisis insurance. Gold has properties that make it a very important portfolio component in certain situations. This will be discussed below.

Gold is an important portfolio component in times of crisis

Gold is an insurance policy for uncertain times. Uncertain times are caused by geopolitical tensions, financial repression and high levels of debt. If a climate of fear arises, this drives up the demand for gold. Conversely, if confidence returns, the demand for gold decreases and the price falls again. The gold quota should therefore not be a fixed value in the portfolio context, but should be actively managed using the following indicators.

Gold and inflation

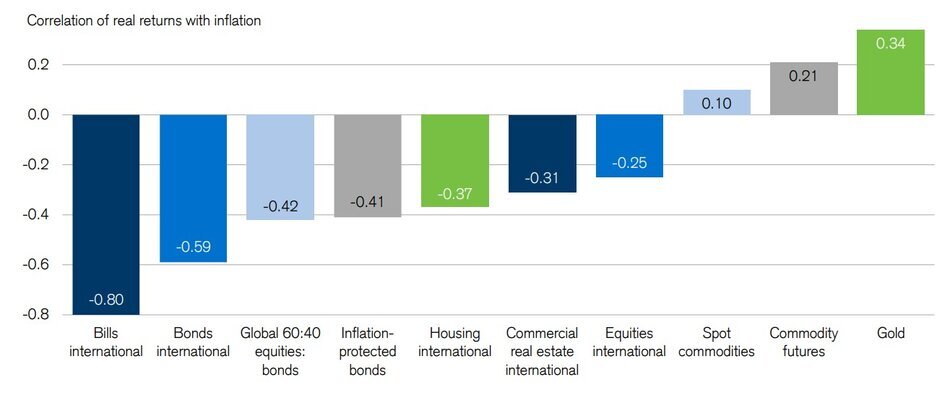

Gold protects the portfolio against currency devaluation caused by an expansionary monetary policy. The following chart shows the correlation between various asset classes and inflation. A negative correlation means that the asset classes concerned lose value when inflation rises. Conversely, a positive correlation means that when inflation rises, the prices of the asset classes concerned rise. A correlation of one would be the complete synchronisation between inflation and the asset class. Gold in USD has a clearly positive correlation with inflation, albeit not a particularly high one. Inflation protection is more pronounced in times of very low interest rates and above-average inflation. Stronger inflation is therefore an indicator in favour of increasing the gold quota.

Gold, interest rates, the USD and the big break in 2022

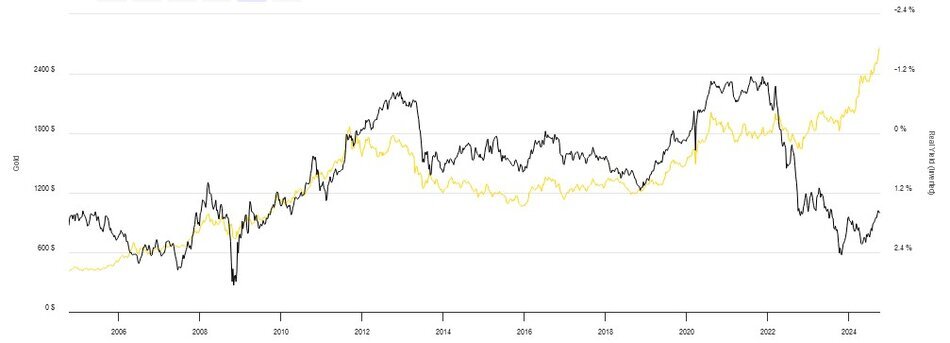

Gold does not generate any income compared to bonds and equities. In phases of low interest rates, gold therefore becomes more attractive compared to interest-bearing securities. Conversely, gold becomes less attractive when safe government bonds yield high interest rates. The same applies to the relationship with the USD. If the USD rises, the price of gold falls and vice versa. The relationship between gold and real interest rates can be illustrated well by placing the development of real interest rates and the gold price development in an inverse relationship to each other (i.e. the scale of real interest rates is shown inversely). The chart below shows that the described relationship between gold and real interest rates worked until 2022. Since 2022, there has been a decoupling of the gold price and real interest rate trends, which is very unusual. The gold price has risen since 2022, even though USD interest rates have also risen. US government securities and short-term money market investments have yielded between 4% and 5% in USD. The gold price should actually have fallen in such an environment.

The reasons for this trend break could lie in the accumulation of other factors that usually drive up the gold price. Two of these factors are debt and sanctions. Both are unfortunately booming and could be the reason why the gold price has risen even though interest rates have also risen.

Gold and debt

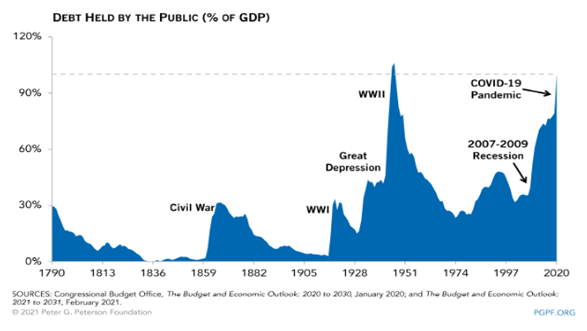

Excessive debt leads to a loss of confidence in currencies. Currencies and the money in circulation are no longer backed by gold, or only to a small extent. The cover is of a factual nature. There is no longer a right to exchange money for gold. The high level of debt is another reason for the attractiveness of gold. Although debt was already very high before Covid, with Covid it has reached levels last seen during the Second World War. In both cases, debt amounted to around 120% of gross domestic product (see chart below):

High debt levels increase the attractiveness of gold, as gold, together with silver, were the precious metals to which currencies were previously pegged.

Gold financial repression and sanctions

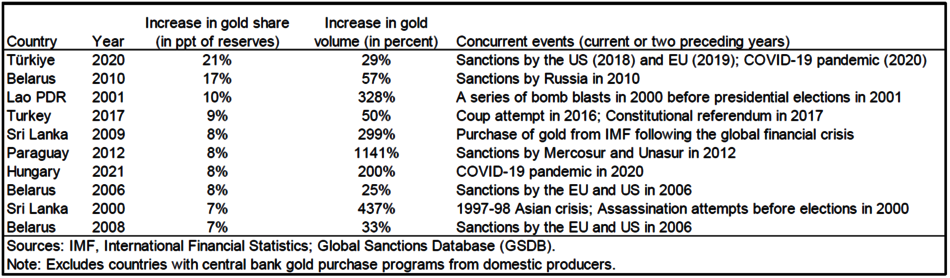

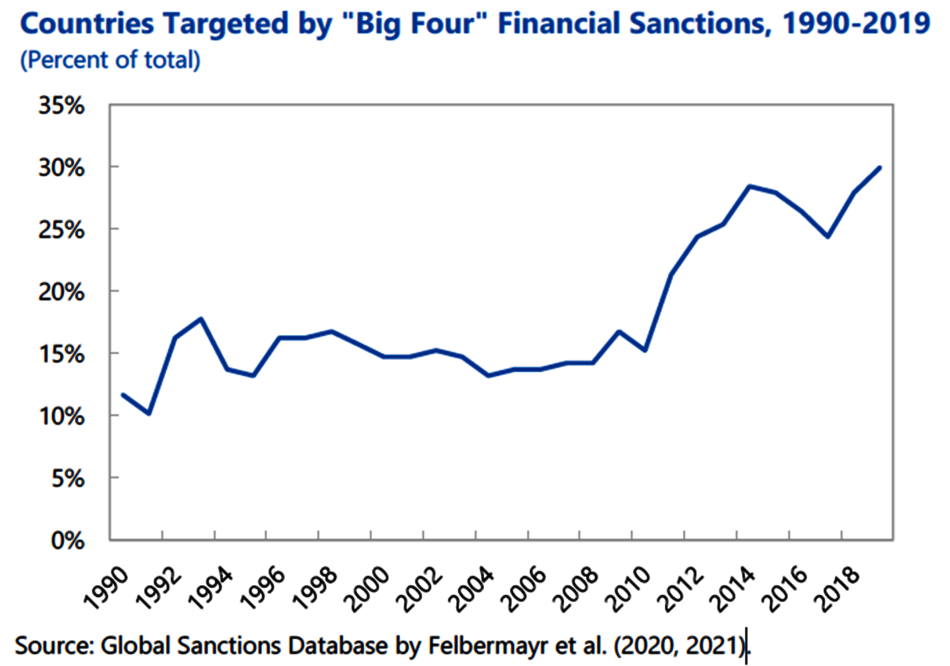

One aspect that is perhaps somewhat overlooked is the influence of sanctions on the gold price. Gold is a reserve currency in times of financial repression and sanctions. If the risk of assets being frozen as part of sanctions increases, gold purchases in the affected countries will rise. Russia, for example, increased its gold purchases after the annexation of Crimea in 2014 and confirmed in 2021 that all gold would be stored in Russia. The advantage of holding gold in reserve is that it can be stored in the home country and is therefore safe from confiscation. The disadvantage is that countries subject to sanctions can only use the gold on the international financial markets to a limited extent. The following list shows the ten largest increases in gold reserves between 1999 and 2021. In half of the cases, gold purchases increased after sanctions were imposed on the country concerned. In the other half of the cases, the increase in gold was linked to political unrest or financial crises.

Sanctions drive up the price of gold, especially when the sanctions are imposed by the "Big Four" (USA, EU, UK and Japan). The rise in the price of gold is much less pronounced when it comes to bilateral sanctions. The following chart shows that the sanctions imposed by the "Big Four" have been on the rise since around 2010.

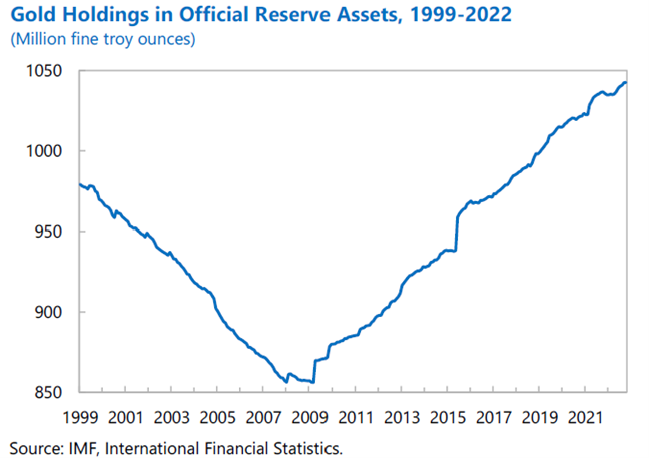

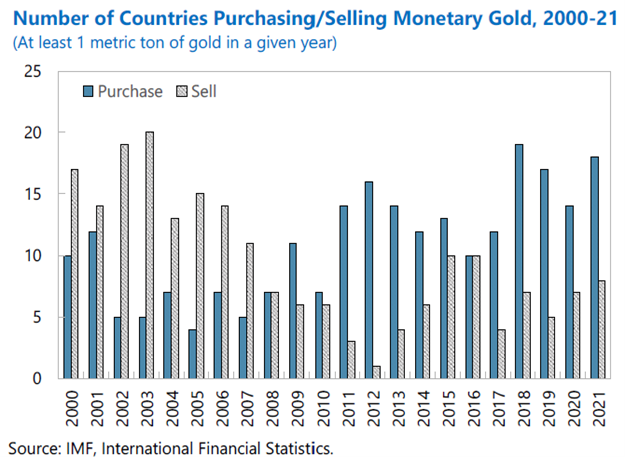

The gold holdings in the public foreign exchange reserves of the major central banks have also increased at roughly the same time as the increase in sanctions. The following charts show that gold reserves have risen sharply since 2010 and that the number of national banks buying gold has been greater than the number of national banks selling gold since 2011. Until 2009, this trend was exactly the opposite. The national banks sold gold.

Sanctions lead to additional gold purchases by the national banks of the affected countries. We live in a world full of sanctions and there is no end in sight. The sanctions against Russia and China have intensified this trend. Further gold purchases by central banks are therefore to be expected. This will have a positive effect on the gold price.

Diversification through a broad basket of commodities

Gold is the classic portfolio diversifier, partly because gold can be held physically. The idea that gold can be brought home from the vault and used in times of crisis is still a reason for the preference for gold and other precious metals. If the use of gold is aligned with the aforementioned developments, it is the right portfolio building block. As already explained, gold has less favourable characteristics from a longer-term perspective. From a longer-term perspective, a broadly diversified portfolio of commodities is the better portfolio component. Diversification within commodities leads to an improvement in returns and a reduction in risk. Gold has an annual real return of 0.76% (geometric mean) or 1.98% (arithmetic mean) per year for the period from 1900 to 2022. For the same period, the real return of an equally weighted basket of 31 commodities is 2.04% (geometric mean) or 2.74% (arithmetic mean) per year. In contrast to the volatility of 17.18% of gold, the volatility of the basket of commodities is only 12.47%. Supplementing gold with other commodities reduces the risk and increases the return. In contrast to gold, such commodity investments must be financially represented and cannot be physically stored locally.

Is investing in gold and commodities ethically justifiable?

There are many reservations about the sustainability of gold and commodities. In our publication "Is it unethical to invest in commodity futures", we analysed the ethical aspects of such investments. We came to the conclusion that trading futures contracts on commodity exchanges has contributed a great deal to the price security of commodities and that historically, bans on such exchanges have increased price fluctuations: to the article by Dr Jonas Steinmann: Is it unethical to invest in commodity futures? In the case of gold, it is important that the origin can be traced and that the extraction of gold is effectively controlled. This means that child labour can be excluded. For these reasons, Invethos uses gold investments that are certified and where it can be assumed that these certifications are correct and complied with on the basis of the producer and the countries of origin.

Conclusions

Gold is a form of crisis insurance and has been an important portfolio component since the gold standard was cancelled. We are currently living in such times of crisis. Debt and inflation are high and an economic war is raging with sanctions. The US Federal Reserve's decision to cut interest rates could give the gold price a further boost. However, more confident times will come when gold positions should be reduced because the fluctuation risk is too high in relation to the return.

Image source: UNSPLASH, photographer: Steve Johnson

Sources

A negative correlation means that when share prices fall, the price of gold rises and vice versa.

For gold, inflation-linked bonds and commercial property, the correlation is only calculated from 1971 (Bretton Woods system abolished)

Swiss Rock Gold